Table of Content

Not affiliated with HUD, FHA, VA, FNMA or GNMA. We work hard to match you with local lenders for the mortgage you inquire about. This is not an offer to lend and we are not affiliated with your current mortgage servicer. The good news is that many banks will remind you when your home equity line of credit is about to move into the second phase. All of our content is authored by highly qualified professionals and edited by subject matter experts, who ensure everything we publish is objective, accurate and trustworthy.

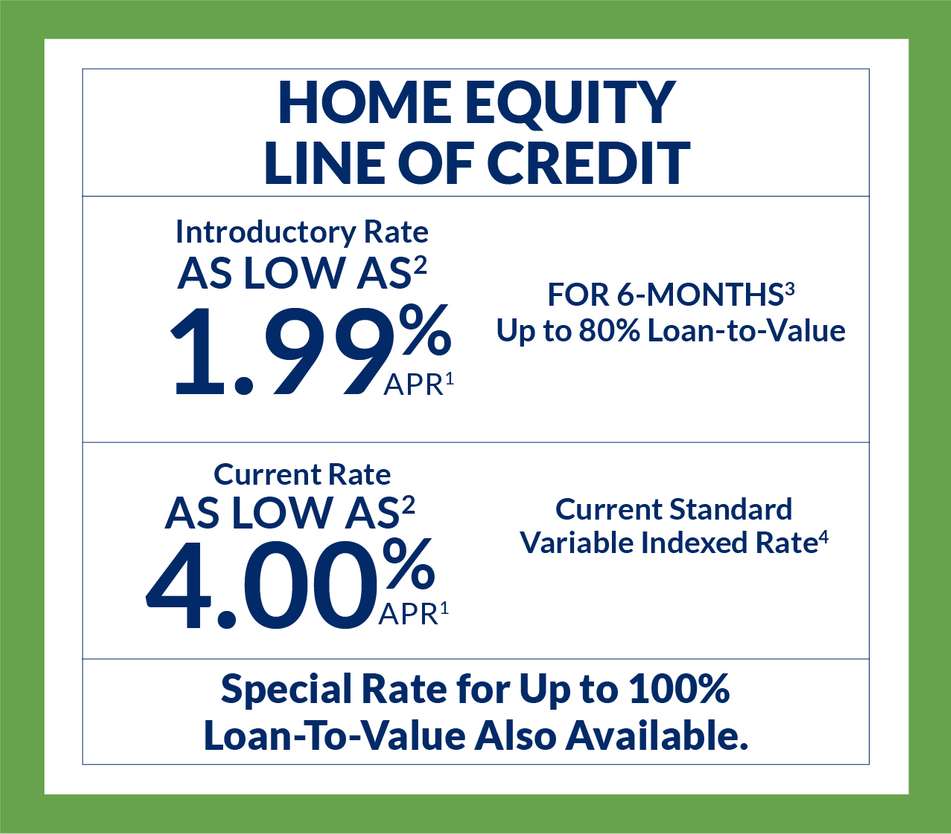

Furthermore, their popularity may also stem from having a better image than a "second mortgage", a term which can more directly imply an undesirable level of debt. However, within the lending industry itself, HELOCs are categorized as a second mortgage. HELOCs are usually offered at attractive interest rates. This is because they are secured against a borrower’s home and thus seen as low-risk financial products. It’s important to contact us as soon as you realize you may have payment challenges.

Option 3: Repayment Period

For example, if an average of index values is used in the plan, averages must be used in the example, but if an index value as of a particular date is used, a single index value must be shown. The creditor is required to assume one date within a year on which to base the history of index values. The creditor may choose to use index values as of any date or period as long as the index value as of this date or period is used for each year in the example. Only one index value per year need be shown, even if the plan provides for adjustments to the annual percentage rate or payment more than once in a year. In such cases, the creditor can assume that the index rate remained constant for the full year for the purpose of calculating the annual percentage rate and payment. Determination of annual percentage rate.

The bank can tell you when the draw period will end, when your repayment term begins, and how much your first payment will be. As your draw period comes to an end, your bank will send you letters reminding you about your repayment terms. “We’re all guilty of not opening every piece of mail, but pay attention to anything coming from your bank,” suggests Giles. The draw period is the predetermined length of time you can use your revolving line of credit.

f) Limitations on Home Equity Plans

We do not cover every offer on the market. Editorial content from NextAdvisor is separate from TIME editorial content and is created by a different team of writers and editors. Take control of your financial future with information and inspiration on starting a business or side hustle, earning passive income, and investing for independence.

Bankrate is compensated in exchange for featured placement of sponsored products and services, or your clicking on links posted on this website. This compensation may impact how, where and in what order products appear. Bankrate.com does not include all companies or all available products.

Convert to a fixed-rate loan

At the end of HELOC repayment periods, borrowers may be allowed to refinance remaining balances or may be required to pay them off completely. HELOC balances can also change on a daily basis, so interest is calculated daily rather than monthly. Use our Early Paydown ProgramSM, which gives qualified borrowers the ability to convert your variable-rate home equity line of credit balance into a fixed rate and fixed term before the end of draw date.

If an initial discount is not taken into account in applying maximum rate limitations, that fact must be disclosed. If separate overall limitations apply to rate increases resulting from events such as the exercise of a fixed-rate conversion option or leaving the creditor's employ, those limitations also must be stated. Limitations do not include legal limits in the nature of usury or rate ceilings under state or Federal statutes or regulations. The interest rate may change from a variable rate during the draw period to a fixed rate during the repayment period. The combination may increase your monthly payments substantially, especially if you made interest-only payments during the draw period.

What happens if I don’t pay my HELOC?

Please review its terms, privacy and security policies to see how they apply to you. Chase isn’t responsible for (and doesn't provide) any products, services or content at this third-party site or app, except for products and services that explicitly carry the Chase name. You may be eligible to refinance your home equity line of credit into a new HELOC which means you would be transferring your current HELOC balance into a new home equity line of credit — with new terms and conditions.

The disclosures could be located on the same Web page as the application without necessarily appearing on the initial screen, immediately preceding the button that the consumer will click to submit the application. When inquiring about a mortgage on this site, this is not a mortgage application. Upon the completion of your inquiry, we will work hard to match you with a lender who may assist you with a mortgage application and provide mortgage product eligibility requirements for your individual situation.

Your draw period is typically a set number of years, often 10 years. When taking out a home equity line of credit , the HELOC draw period is your chance to spend the money you borrow before you have to pay it back. It’s the first step once you’ve closed on your HELOC, a flexible way to borrow against the equity you’ve built up in your property.

HELOCs are typically variable-rate loans, meaning the interest rate you pay is based on the market and reset every so often. During the draw period, you typically have to make minimum payments on the loan, which can often be interest-only. At the end of the draw period, you may be able to renew your line of credit and restart the clock. Otherwise, you’ll enter the repayment period of the loan. A creditor may change the annual percentage rate for a plan only if the change is based on an index outside the creditor's control.

A creditor also may provide in the initial agreement that specified changes will occur if a specified event takes place (for example, that the annual percentage rate will increase a specified amount if the consumer leaves the creditor's employment). The historical example must reflect all features of the repayment period, including the appropriate index values, margin, rate limitations, length of the repayment period, and payments. For example, if different indices are used during the draw and repayment periods, the index values for that portion of the 15 years that reflect the repayment period must be the values for the appropriate index.

The change must be agreed to in writing by the consumer. Creditors are not permitted to assume consent because the consumer uses an account, even if use of an account would otherwise constitute acceptance of a proposed change under state law. A limitation on automated teller machine usage need not be disclosed under this paragraph unless that is the only means by which the consumer can obtain funds. In lieu of the disclosure required under paragraph of this section, a statement of such conditions. A statement that the consumer should make or otherwise retain a copy of the disclosures.

During a HELOC's draw period borrowers generally only have to make interest, not principal, payments on the money drawn from them. This will give you an entirely new HELOC with a new interest-only draw period. You will still have a line of credit, but you will be responsible for eventually paying off the balance.

No comments:

Post a Comment