Table of Content

Most payments during the draw period are interest-only payments. An explanation of how the annual percentage rate will be determined, including an explanation of how the index is adjusted, such as by the addition of a margin. The fact that the annual percentage rate, payment, or term may change due to the variable-rate feature. A statement that negative amortization may occur and that negative amortization increases the principal balance and reduces the consumer's equity in the dwelling. The disclosures required under this section need be made only as applicable.

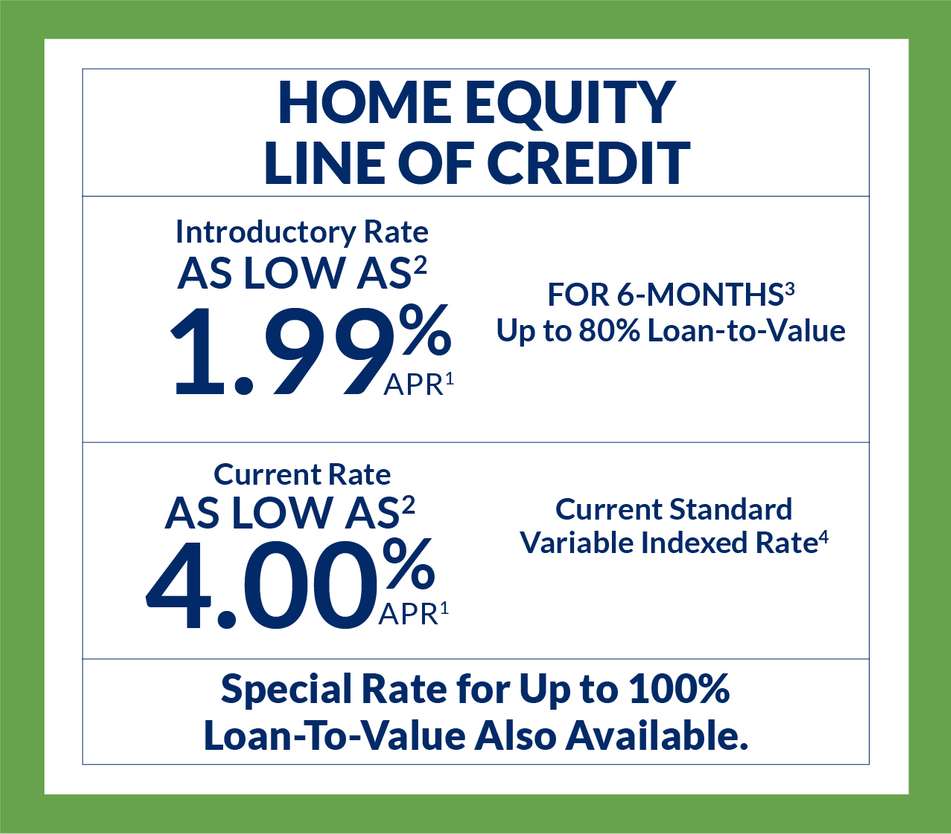

A borrower is approved for a specific credit limit and can draw on those funds up to the limit as needed during the draw period, making monthly payments as required according to the signed contract. For a home equity line of credit, end of draw is the point at which you can no longer access funds. Most lines of credit have a 10-, 15-, or 20-year draw period and then move into the repayment period, when you’ll repay your outstanding balance with full principal-and-interest payments.

Know your end of draw balance and end of term date

Weigh the pros and cons of each option before making a decision. For example, when you refinance into another HELOC, you could incur additional costs, such as early closure fees, annual fees and application fees. Before your HELOC draw period ends, have a repayment plan in place if you owe money. Check with your lender to see exactly how much your monthly payments will change once the principal portion is due. Depending on how high your remaining balance is before the draw period ends, your monthly payments in the repayment period could be a financial shock.

As a result, lenders generally require that the borrower maintain a certain level of equity in the home as a condition of providing a home equity line, usually a minimum of 15-20%. Make sure you’re prepared for any financial challenges before your home equity financing enters end of draw or end of term status. Our specialists are ready to help you understand your options. Chase's website and/or mobile terms, privacy and security policies don't apply to the site or app you're about to visit.

What can I do to reduce my monthly payment at the end of draw period?

If the creditor adjusts its index through the addition of a margin, the disclosure might read, “Your annual percentage rate is based on the index plus a margin.” The creditor is not required to disclose a specific value for the margin. Some reverse mortgages provide that some or all of the appreciation in the value of the property will be shared between the consumer and the creditor. The creditor must disclose the appreciation feature, including describing how the creditor's share will be determined, any limitations, and when the feature may be exercised. A fixed interest rate can be a good idea if you think you’ll need the entire repayment period to pay off the HELOC. It will give you predictable monthly payments so you can budget accordingly. However, a variable interest rate may be better for some borrowers.

“Repayment periods are completely dependent on the lender,” says Mazzara. “I’ve seen 20-year lines, 15-year lines, five-year lines. I’d say the average is about 15 years,” she says. After several years of making interest-only payments, the jump to full interest and principal payments can come as a shock, so make sure you review your loan documents and make note of when your HELOC will enter repayment. “Be prepared to make that full payment when the loan converts to a fully amortized payment schedule,” says Tabitha Mazzara, director of operations with the Mortgage Bank of California . Minimum credit ratings may vary according to lender and mortgage product.

OPEN AN ACCOUNT

“It can be a switch,” says Katie Bossler, Quality Assurance Specialist at GreenPath Financial Wellness, a national nonprofit financial counseling agency. “It’s kind of like having a credit card that’s no longer available for use,” she adds. When you qualify for a home equity line of credit, or HELOC, you'll usually be given a multi-year draw period for it. Draw period lengths themselves vary depending on the loan terms of any particular HELOC. After the end of your HELOC's draw period, you become responsible for making payments on it.

Any mortgage product that a lender may offer you will carry fees or costs including closing costs, origination points, and/or refinancing fees. In many instances, fees or costs can amount to several thousand dollars and can be due upon the origination of the mortgage credit product. Once your HELOC's draw period expires, you'll be unable to access any remaining approved loan amounts. Also, you're not obligated to draw the entire HELOC loan amount before the draw period expires. Once your HELOC's draw period ends, you must repay only the funds you took out, not your approved loan amount. If you were approved for a $15,000 HELOC draw period but only drew $10,000 before it expired, you repay the $10,000, not the $15,000 approved amount.

When you want to access the money, you write out a check. You make the check payable to either the recipient or to cash, in which case you can deposit it into your personal checking account. Other options besides a check include a credit card or online transfer capability. Depending on the bank, you will have between five and 10 years to access the money. If you pay back the principal balance at any time, that money will become available to you again. It’s important to know that you don’t have to wait for the repayment period to start making payments.

In transactions where the minimum payment will not or may not be sufficient to cover the interest that accrues on the outstanding balance, the creditor must disclose that negative amortization will or may occur. This disclosure is required whether or not the unpaid interest is added to the outstanding balance upon which interest is computed. A disclosure is not required merely because a loan calls for non-amortizing or partially amortizing payments.

Now that the term has ended, the outstanding balance is due in full, and a substantial lump-sum balloon payment may be required. HELOCs generally have variable interest rates, but some lenders will allow you to convert some or all of the amount you borrow to a fixed-rate loan. This has the advantage of locking in your monthly payment, so you don’t have to worry about it rising over time. Keep in mind, however, that some lenders require you to choose this option before the end of the draw period. Any additional principal payments made during the draw period on a HELOC will reduce the payments due during the HELOC's repayment period. During the draw period, your online account through your HELOC servicer should show you estimates of what your monthly payment will be during the repayment period.

Matthew has been in financial services for more than a decade, in banking and insurance. The offers that appear on this site are from companies that compensate us. This compensation may impact how and where products appear on this site, including, for example, the order in which they may appear within the listing categories. But this compensation does not influence the information we publish, or the reviews that you see on this site.

No comments:

Post a Comment